Voice of the Buyer AI Research Reality Check: From Hype to Proof

11 min

Updated: July 27, 2026

Thank you!

Your report is available now

UNLOCK THE FULL REPORT

Introduction

INFUSE Voice of the Buyer 2026 revealed the Trust Gap as the defining condition of B2B buying in 2026: despite more access to information than ever from vendors, buyer confidence in their purchase decisions is at an all-time low.

Six months later, AI sits at the center of every B2B buying decision. While the market continues to debate the future of the technology, buyers are pragmatically evaluating AI solutions for risk, without losing sight of quarterly outcomes.

When weighing this risk, B2B buyers are evaluating standalone AI-first solutions, agentic deployments, and AI capabilities embedded inside existing platforms in their tech stack. This technical complexity, combined with rising costs, infrastructure changes, and the challenge of upskilling teams, is driving buyers to scrutinize AI solutions against proven outcomes, moving beyond the novelty of the AI itself.

This VOB research update measures what has changed for B2B enterprise buyers as they shift from early, experimental AI adoption into structured evaluation and deployment.

This mid-year research, based on responses from 310 enterprise business and technology professionals, confirms a shift from hype to proof. B2B buyers who are charged with identifying, assessing, and purchasing solutions are trying to cut through the noise and more thoroughly evaluate AI across four core criteria:

- Integration with existing tech stacks

- Quantifiable ROI from comparable use cases

- Plain language on what AI solutions actually provide

- Guardrails and governance to deploy AI responsibly

Tech stacks are consolidating in response, with every vendor renewal re-justified against a single comparison: buyers are evaluating the value of AI functionality inside the platforms they already use (often from legacy vendors), compared to new, AI-first providers and solutions.

This shift places AI-first trailblazers and established legacy vendors on the same battleground, with legacy vendors still benefiting from established trust when integrating AI into known solutions.

Vendor Hype

AI promises dominated technology marketing and product roadmaps. Partnership ecosystems and digital transformation 2.0 collide with unproven AI claims across categories, intensifying buyer scrutiny.

Buyer Urgency

Pressure to invest rapidly. AI becomes the top investment focus as the growth-at-all-costs era ends, as organizations sought productivity, growth, and competitive advantage. Many buying groups accelerated evaluations, committing faster than vendors can prove outcomes.

Operational Efficiency

Buyers anchor AI evaluations on operational efficiency and ROI to meet performance requirements. Confidence declines despite information abundance, with technology adoption outpacing organizational readiness, expertise, and alignment across the buying group.

Deliberate Evaluation

The Trust Gap persists. Buying groups convert skepticism into structured evaluation that tests three key elements: integration with the existing stack, quantified returns from comparable clients, and transparency about what AI does. Tech stacks are consolidating; purchases are determined by business case fit, whether or not AI is involved.

“The first wave of AI buying was driven by fear of missing out. The second is driven by the discipline of business cases. Buyers are still moving, but they are moving on their terms, with proof of outcomes as the price of entry.”

Founder & CEO, INFUSE

This mid-year update covers:

Research themes

2026 Q2 trends

Buyers are scrutinizing every vendor in their stack

- AI is forcing every recurring contract vendor to re-justify its value and place in the tech stack

- SaaS consolidation is underway, with established vendors gaining ground over AI-native entrants among enterprise buyers

Integration and transparency separate winners from challengers

- Integration with target buyers’ existing stack is the new shortlist test

- Transparency and quantified outcomes have replaced brand, novelty, and roadmap as the vendor proof tier

Augmentation, not transformation, is the operating assumption

- AI is changing the speed of buying decisions but not the underlying process

- Buying groups, cycles, and consensus requirements remain intact

Audience overview

Buyers are scrutinizing every vendor in their stack

The competition to earn and retain a place in the technology budget has intensified with the rise of AI. INFUSE forecasted the first wave of this pattern in the Great Tech Stall, when buyers retrenched after the 2020 to 2023 digitization surge and trimmed accumulated SaaS subscriptions.

The 2026 deceleration is sharper: buyers continue to invest in technology, with each recurring fee for a new solution weighed against the AI capabilities they could acquire within an existing platform or build internally.

The calculation increasingly favors solutions B2B buyers already have, with risk, governance uncertainty, and the pace of AI capabilities shifting within incumbent platforms driving the change.

Operational efficiency dominates the AI agenda, with strategic applications trailing close behind

What is the primary outcome you are looking to achieve by applying AI within your organization?

Answer option

% of respondents

Operational efficiency: streamlining workflows and lowering operational costs

62%

Automation: reducing manual tasks and accelerating routine processes

51%

Innovation: enabling new capabilities or approaches not previously possible

36%

Revenue growth: directly improving sales, pipeline, or customer acquisition

33%

Competitive positioning: keeping pace with or gaining advantage over competitors

12%

- Efficiency and automation set the operating frame: Operational efficiency (62%) and automation (51%) tower above other outcomes, confirming that buyers frame AI first as a way to do existing work better, not as a route into new territory.

This pattern repeats earlier trends in INFUSE research demonstrating operational efficiency as the top desired outcome across technology investments (41% in 2025, 31% in 2026), with AI specifically intensifying the same focus (INFUSE Voice of the Buyer 2026). - Innovation outranks revenue growth: Innovation (36%) sits ahead of revenue (33%), indicating that buyers are interested in new capabilities but prioritize near-term efficiency gains.

Innovation is funded only after the cost base is defended.

- Competitive positioning ranks last: At 12%, buyers treat AI as a baseline expectation rather than a differentiator. The pattern reflects an organizational reality. Most buyers are still building the internal capability, governance, and proof points to operationalize AI at all, and competitive positioning is the last priority funded after those foundations land.

Takeaway

Buyers are anchoring AI investments to operational gain.

AI narratives built around transformation rhetoric miss the audience. Vendors that map AI capability to specific cost-side and productivity outcomes, then quantify the lift, earn budget conversations that others do not.

The efficiency-first frame is consistent with INFUSE Outlook 2026, but it carries a risk the data does not show: automating or accelerating a process without quality guardrails degrades every decision it informs. Buyers focused only on efficiency absorb this risk by default.

The vendors winning long-term contracts show buyers how to pair efficiency gains with the guardrails that protect decision quality.

“Efficiency is the way in, not the destination. The vendors quantifying hours saved and workflows tightened earn the meeting. The ones helping buyers see how those savings fund growth, instead of just running broken processes faster, earn the relationship.”

Chief Commercial Officer, INFUSE

SaaS consolidation underway, with AI as the catalyst

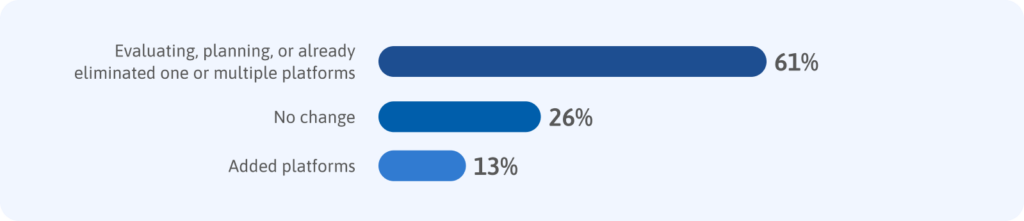

How has AI influenced the number of SaaS platforms your organization uses in the past 12 months?

- The consolidation movement dominates the response: 61% of buyers are evaluating, planning, or have already eliminated one or more platforms because of AI, against 13% adding platforms.

For every buyer expanding the stack because of AI, more than four are contracting it.

“I built an ERP solution in less than a week: fully hosted, with OCR recognition, inventory management, embedded forecasting and scenario modeling. It serves my needs at the moment.”

CEO, Manufacturing, NAM

- The risk of churn is high: Earlier INFUSE research found that 48% of buyers were somewhat satisfied with vendors and 21% were neutral, masking the real churn risk in the satisfaction scores (INFUSE Voice of the Buyer 2026). This research update shows that risk is solidifying, with buyers cutting where loyalty was passive rather than earned.

Takeaway

Renewal is the new sales motion.

Every recurring contract competes against the question of what AI inside an adjacent platform delivers for the same budget. Vendors that fail to demonstrate unique, AI-augmented value at renewal lose clients.

Vendors that make AI guardrails, output ownership, and renewal criteria easy for the buyer to apply cement their positioning. The seller-side consolidation pressure is well documented, with 54% of enterprise CIOs actively running vendor-consolidation programs (a16z 2025 CIO survey).

For vendors prospecting net-new logos, renewal economics define what it takes to displace an incumbent: net-new acquisition now requires evidence that the AI capability solves a specific problem that the buyer’s current stack cannot, backed by quantified outcomes from comparable clients and a clean integration path. Without clear proof from the new vendor, the incumbent’s AI roadmap is enough to defer the sales conversation indefinitely.

Buyers evaluate on merit, with established vendors winning five to one when a preference is declared

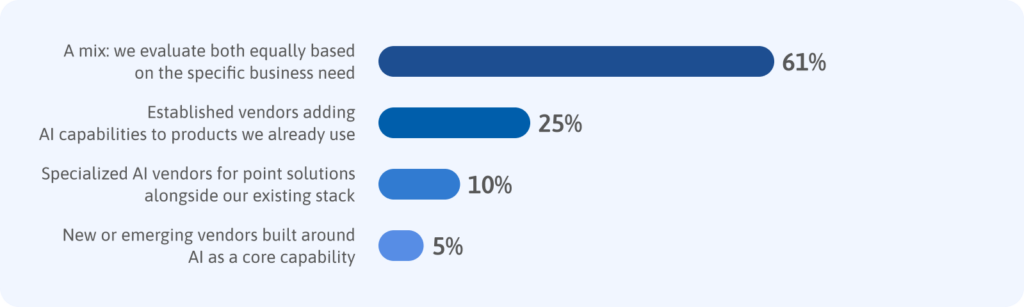

When evaluating AI-powered solutions, which type of vendor does your organization lean toward?

- Pragmatism leads: A clear majority (61%) evaluates established and AI-native vendors on the merits of the specific need rather than defaulting to one type. Buying is case by case, not category by category, with the largest single group refusing to anchor to either incumbent or insurgent.

- Established vendors win the preference battle: Where buyers express a preference, established vendors adding AI capability outdraw AI-native entrants 25% to 5%, a five-to-one margin.

The finding confirms earlier INFUSE research showing brand familiarity very or extremely influential for 45% of buyers (INFUSE Voice of the Buyer 2026); familiarity converts directly into shortlist position when AI enters the conversation. - AI-native vendors face a trust headwind: Among the 39% of buyers who declare a preference, only 5% default to AI-native entrants. Two reinforcing dynamics explain the gap: AI-native vendors are still emerging into enterprise category presence, and most buyers do not yet have enough AI experience to know what to ask of them. Until both gaps close, novelty alone will not be a strong selection driver.

Takeaway

Established vendors that embed credible AI features into trusted products are running a structural advantage, while AI-native vendors must compete with irrefutable evidence.

Familiarity acts as a risk-reduction shortcut buyers reach for when AI introduces fresh uncertainty into an already complex evaluation. The pattern is visible in the broader market, with legacy infrastructure and enterprise platform vendors reporting record sales on the back of AI tailwinds (as of June 2026, Microsoft’s AI business increased 123% year-over-year; Salesforce’s Data Cloud and AI ARR increased 120%).

AI-native vendors win where they can prove a step-change capability over what the incumbent already offers. Everywhere else, the incumbent secures the renewal.

“The buyer is anti-risk. AI-native vendors that show up with proof points, customer references, and clean integration paths can absolutely win, but the bar is higher than the incumbent’s because the unknowns are larger.”

Chief Market Officer:

GTM Executive and

Advisor to CXOs & Teams

Integration and transparency separate winners from challengers

Consolidation reframes the budget question; integration and transparency reframe vendor evaluation.

Buyer questions have moved past whether a vendor has AI and into specifics about how the AI behaves inside the stack, what data it touches, and where it fails. The same shift appears in a broader sample of third-party data, with more than 60% of business buyers running product trials before committing (Forrester, 2026).

Proven integration is the dominant evaluation criterion

In a market where nearly every vendor now claims AI readiness, what do you prioritize most when evaluating an AI-powered solution?

Answer option

% of respondents

Proven integration with our existing technology environment

47%

Evidence of measurable business outcomes from current clients

32%

Transparency about what the AI actually does and its limitations

23%

Depth of AI capability versus surface-level AI features

13%

The vendor’s track record and reputation, independent of AI claims

12%

Validation from peers, independent reviews, or third-party sources

4%

- Integration is the gate: Proven integration tops the list at 47%, well ahead of every other factor. Business and tech leaders want AI to work alongside their core software platforms, with evaluation focused on layering AI capability onto the stack they already run. The threat falls on vertical SaaS tools, as well as one-off task subscriptions that agentic AI can already replicate inside platforms a buyer already runs. Integration with the core stack becomes the protection that incumbents negotiate from.

- Proof and transparency anchor the next tier: Measurable outcomes (32%) and transparency about what the AI actually does (23%) sit close behind, confirming a Trust Gap that demands evidence and honesty over claims. The same Trust Gap is documented externally, with buyer trust in vendor AI ethics falling from 58% to 42% between 2023 and 2025, and 71% of buyers wanting a human to validate AI outputs (Salesforce, 2025).

- Third-party validation ranks lowest: Peer or third-party validation at 4% ranks lowest, reflecting the early-stage nature of AI solutions rather than a lack of industry emphasis on reviews. Buyers are evaluating in private, treating external validation as confirmation rather than discovery, with 73% of the B2B buying journey now happening anonymously before any vendor contact (6sense, 2025).

Takeaway

Integration is the new shortlist test.

Vendors that lead with feature depth before establishing integration credibility risk dissuading potential buyers in the early stages of their evaluation process.

The shortlist test in 2026 is whether the AI fits into the buyer’s stack. Integration now operates as the qualifier, the test that determines whether vendors enter the evaluation at all. The finding aligns with the 58% of buyers who ranked strong alignment with use case, technical requirements, or existing stack as a top shortlist factor in earlier INFUSE research (INFUSE Voice of the Buyer 2026).

“Buyers are still asking what your AI does. What has changed is what counts as an answer. They want a technical description that gets approval from the engineer in the room, not a brand statement. The CMOs winning this cycle are the ones marketing the integration and outcomes, not the AI.”

CMO, INFUSE

AI vendor selection is decided by problem fit and ROI, with embedded AI winning over standalone features

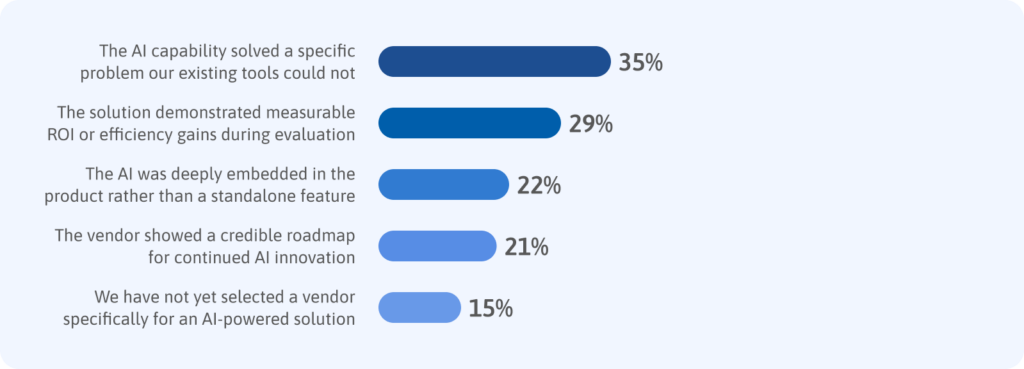

When you have selected a vendor specifically for an AI-powered solution, what was the primary reason?

- Outcome-led selection prevails: Solving a specific problem existing tools could not (35%) and demonstrating measurable ROI during evaluation (29%) are the two leading reasons for selection, confirming an outcome-led rather than feature-led buying motion.

- Embedded beats standalone, with roadmap close behind: 22% selected because AI was embedded in the product rather than simply added on, with a credible roadmap for continued AI innovation a close second at 21%. The pairing signals that buyers weigh current embedding and future trajectory in balance, and aligns with earlier findings revealing innovation as the most unmet outcome from current vendors at 34% (INFUSE Voice of the Buyer 2026).

- More than one in seven has not selected an AI vendor: 15% have not yet committed to an AI-specific vendor and are building AI capability internally before evaluating external solutions. The group represents a near-term delay risk for vendors and a future opportunity for those that can show AI capability the internal team cannot replicate.

Takeaway

Show buyers a specific problem solved with quantified ROI, or expect to lose the evaluation before features are even discussed.

The vendor evaluation has shifted from product capability to differential capability. Buyers now look for AI that does something they cannot replicate in-house, and vendors that answer with embedded AI capabilities tied to quantified outcomes (hours saved per workflow, cost per task, revenue per rep) win the conversation.

Vendors that lead with AI as a top-level feature on a slide invite the comparison to internal builds and lose. The pressure to quantify cuts both ways: only 41% of marketers can confidently prove AI ROI today, down from 49% in 2025. Yet, where ROI is measured, most organizations report 2x or greater returns (Jasper State of AI in Marketing 2026). Buyers want the proof that their own internal teams are still struggling to produce.

“The AI deals closing fastest in 2026 are the ones where vendors prove an outcome the buyer cannot produce in-house, then translate that outcome into a number the CFO already recognizes. Proof has replaced promise.”

Founder & CEO, INFUSE

Augmentation, not transformation, is the operating assumption

Most vendor messaging in 2026 assumes AI is transforming how buyers buy. The data says otherwise.

Across multiple questions, buyers describe AI as accelerating discovery, sentiment, and personal proficiency, while leaving the structure of the evaluation process intact.

The buying group still expands, the cycle still requires consensus, and the proof points still matter. However, the category of work AI changes turns out to be smaller than the category vendors assume.

AI urgency is uneven, with some categories accelerating and others taking longer to deliberate

Has the emergence of AI affected the urgency of your technology buying decisions?

Answer option

% of respondents

Yes, some categories are moving faster while others require more deliberation

38%

No, the pace and urgency of buying decisions have remained consistent

33%

Yes, buying cycles have shortened as teams are under pressure to adopt AI sooner

18%

Yes, buying decisions are lengthier as the risk of selecting the wrong solution increases

12%

- AI adoption is not accelerating uniformly: Instead, 38% of buyers report fast-tracking some categories while taking a more measured approach to others, making category-level analysis essential to understanding purchasing behavior.

- A third report no change: 33% see no shift in pace, a larger steady-state group than industry narratives about AI-driven acceleration would suggest.

- Faster and slower roughly cancel: Shortened cycles (18%) and lengthened cycles (12%) offset one another, reinforcing the split-by-category finding. The average cycle dropped from 8 to 7 months in 2026, attributed in part to AI pressure (INFUSE Voice of the Buyer 2026). This AI Update survey refines the picture by showing the acceleration concentrated in specific categories rather than spread across the board.

Takeaway

AI-driven urgency is specific, not universal.

Vendors selling in AI-adjacent categories, including content, analytics, and process automation, should expect faster cycles. Vendors selling in categories where AI introduces material implementation risk should expect longer cycles and more stakeholders. Both responses are occurring simultaneously, and segmentation matters more than ever.

“There is no point automating everything. We identify the pain points and automate those only. But the technology moves so fast that by the time we decide what to build, the platform we wanted to build it on is already outdated. And the committee approving the project has never touched the technologies they are approving.”

Senior Technical Lead,

Healthcare Technology, NAM

Workplace AI sentiment is broadly optimistic

Which of the following best describes your personal sentiment toward AI in the workplace?

Answer option

% of respondents

Optimistic: a clear opportunity for professional growth and improved performance

50%

Cautiously optimistic: I see the potential but have uncertainty about the impact

23%

Neutral: I do not have a strong view in either direction

21%

Concerned: I have reservations about the impact on roles, skills, or ways of working

6%

Opposed: I believe AI introduces more risk than value

1%

- Optimism dominates: 73% of respondents are optimistic or cautiously optimistic, indicating a broadly positive disposition toward AI at work. This is consistent with the wider workforce, where 66% of employees express similar optimism about AI in the workplace (Ruder Finn, 2025).

- Resistance is limited: Active resistance is not a meaningful factor within this audience of B2B technology buyers.

- One in five remains undecided: The neutral group (21%) represents respondents forming a view in a rapidly moving environment, a useful target for education-focused engagement.

Takeaway

The business technology buyers are leaning in, not pushing back.

Vendor messaging that treats buyers as AI-skeptical underestimates the room. The friction in B2B AI buying is not philosophical resistance to the technology. It is practical caution about specific solutions, vendors, and use cases. That distinction shapes how vendors should frame the conversation.

“Optimism is the starting condition, not the outcome. Operating teams convert it into adoption when there is clear ownership, governed workflows, and measurable outputs. Without that infrastructure, sentiment dissipates into another year of pilots, and the vendors that help operations teams build that scaffolding are the vendors that get scaled.”

COO, INFUSE

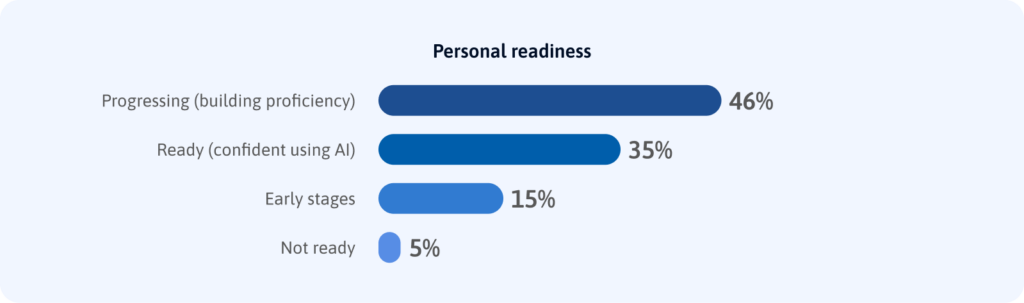

Personal AI readiness runs ahead of organizational readiness

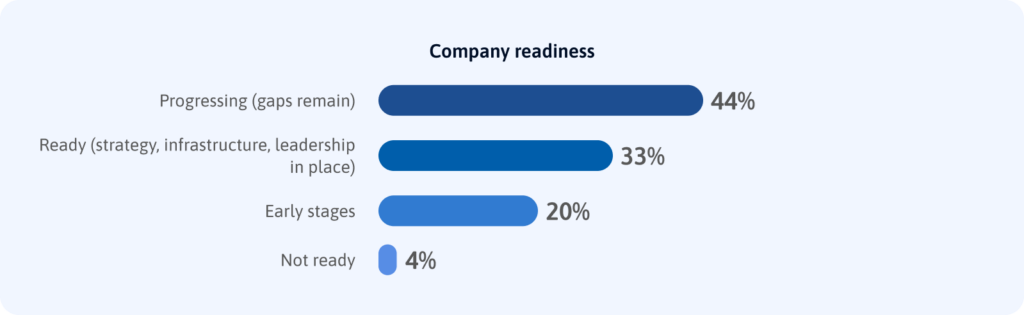

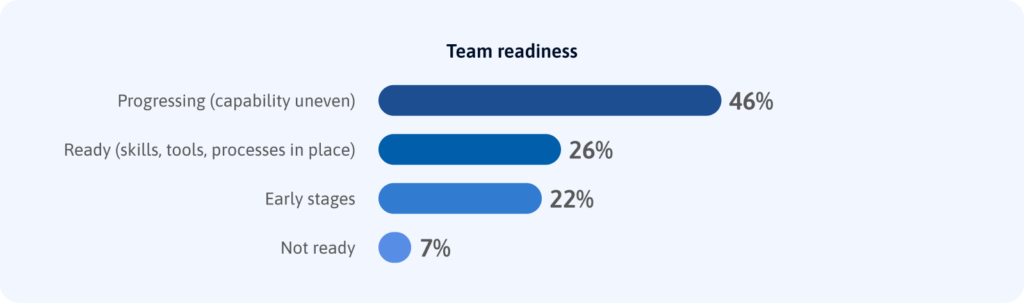

How would you rate the level of AI readiness across your company, team, and personal usage?

- Progressing is the dominant state at every level: Across company (44%), team (46%), and personal (46%) views, the same near-half share reports active transition rather than full readiness or non-engagement.

- Individual readiness leads organizational readiness: People feel further along personally (35% ready) than they judge their organizations (33%) or their teams (26%). The same pattern repeats outside the buyer audience, with 63% of marketing organizations at intermediate or advanced AI maturity but only one in three marketers carrying formal AI responsibility in their role (Jasper State of AI in Marketing 2026). Individuals are operationalizing AI faster than their organizations are restructuring around it.

- “Not ready” is consistently small: Under 8% at every level. The question for this audience is the pace of maturation, not whether to begin exploring AI tools.

Takeaway

The readiness gap between people and the organizations they support is now a vendor opportunity.

Buyers who feel personally ready are running ahead of their employers and looking for vendors that can close the gap. Solutions that enable individuals to demonstrate AI value internally, then scale that value across teams and the wider business, find a receptive audience already primed to act.

“The fastest path to organizational AI adoption is the user who already knows what good looks like. Vendors that empower the practitioner, not just the platform owner, are unlocking the budget conversations earlier.”

VP Global Client Success

and Strategy, INFUSE

AI augments the evaluation process; it does not replace it

As of today, how do you expect AI to change the way your organization evaluates and selects technology vendors?

Answer option

% of respondents

AI will play a growing role but our core evaluation process will remain largely the same

41%

It is too early to tell; there is too much uncertainty to predict how AI will affect our selection process

27%

AI will fundamentally change our selection process; we expect to use AI as a primary research method

18%

AI will have little impact; we expect to evaluate vendors the same way we do today

14%

- Augmentation is the leading view: 41% expect AI to play a growing role while the core evaluation process remains largely the same, making augmentation the single dominant answer. A further 27% say it is too early to predict how AI will affect selection, suggesting many buyers are still working through implementation specifics rather than questioning whether AI changes evaluation at all.

- Fundamental change is the minority view: Only 18% expect AI to fundamentally change selection, and 14% expect little impact. Both ends of the spectrum sit well below the augmentation answer, tempering expectations of either radical change or business-as-usual.

- AI augments but does not replace research: Earlier INFUSE data showed that AI tools or agents were used as a vendor-research source by only 4% of buyers in 2025, and AI summaries ranked low at the identify-need stage (INFUSE Voice of the Buyer 2026). The augmentation view holds: AI compresses discovery without removing the human evaluation steps that follow.

Takeaway

The buying process is being augmented, not rewritten.

Vendors that own the categories buyers’ research, publish substantive content, and prove integration with the existing stack will continue to win. AI compresses the path to that win rather than removing it.

The stakes have risen accordingly, with 94% of buyers now using LLMs during their buying journey and 95% forming a shortlist before any seller contact, where the pre-contact favorite wins 80% of deals (6sense, 2025). AI changes the speed of discovery while leaving the underlying requirement in place: vendors still have to be found, trusted, and shortlisted before the conversation starts.

Key takeaways

- Tech stack scrutiny is the new sales motion: Six in ten buyers are cutting platforms or evaluating what to replace. Renewal is no longer the safe baseline; it is the next competitive evaluation. Vendors that fail to prove unique, AI-augmented value at the renewal lose the seat. The pattern echoes the Great Tech Stall INFUSE forecasted in 2024, sharpened by AI as the new consolidation catalyst.

- Integration and transparency are the qualifiers, with proof essential for securing buy-in: Integration with the existing stack is now the dominant evaluation criterion (47%), with measurable outcomes from current clients (32%) and transparency about what the AI actually does (23%) anchoring the next tier of evaluation. Vendors pitching AI capability in isolation lose ground to vendors who can describe how that capability lands inside the buyer’s stack and produces a quantified result.

- Augmentation is the operating assumption, with discoverability as the deciding factor: 41% of buyers expect AI to play a growing role while the core evaluation process stays largely the same, making augmentation the single leading view. A further 27% believe that it is too early to predict the impact. The vendors that win are the ones built into the buyer’s research before AI compresses the path to shortlist.

“Marketers cannot afford to wait for the AI buying playbook to stabilize before they act. The winning approach is to prove integration before the buyer raises the question, quantify the outcome in language a CFO already recognizes, and build presence in the categories buyers research, all before AI compresses the path to shortlist. The vendors winning in 2026 are not the loudest about AI but the ones already inside the buyer’s research at the moment AI accelerates the decision.”

Founder & CEO, INFUSE

BRIDGE THE TRUST GAP AND CONVEY VALUE TO TODAY’S B2B BUYERS

INFUSE demand experts analyze your organization and GTM strategy, recommending the best approaches to build trust with target buyers and grow pipeline.

FAQs

Are B2B buyers consolidating their tech stacks because of AI?

B2B buyers are consolidating their tech stacks, with 61% actively evaluating, planning, or already eliminating platforms as AI alternatives emerge. One in four buyers (25%) has already cut at least one platform, while only 13% have added platforms because of AI. The consolidation movement outpaces expansion by more than four to one, sharpening the churn risk previously surfaced in INFUSE Voice of the Buyer 2026.

Do B2B buyers prefer established vendors or AI-native startups for AI solutions?

When B2B buyers express a preference for AI solutions, they choose established vendors over AI-native startups by a five-to-one margin (25% vs. 5%), while most (61%) evaluate both equally based on the specific business need. The pattern confirms that brand familiarity acts as a risk-reduction shortcut, with 45% of buyers rating familiarity very or extremely influential in INFUSE Voice of the Buyer 2026.

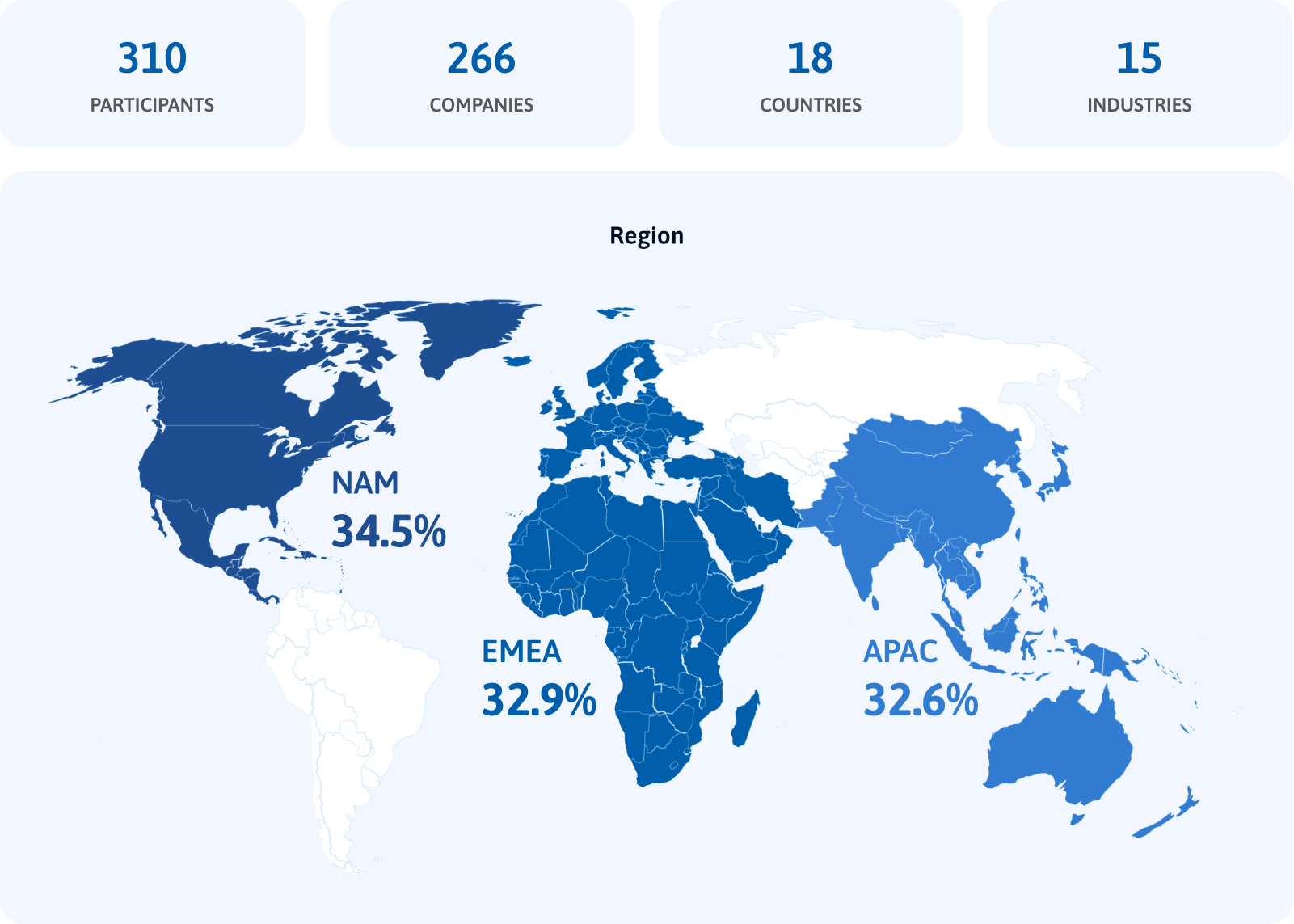

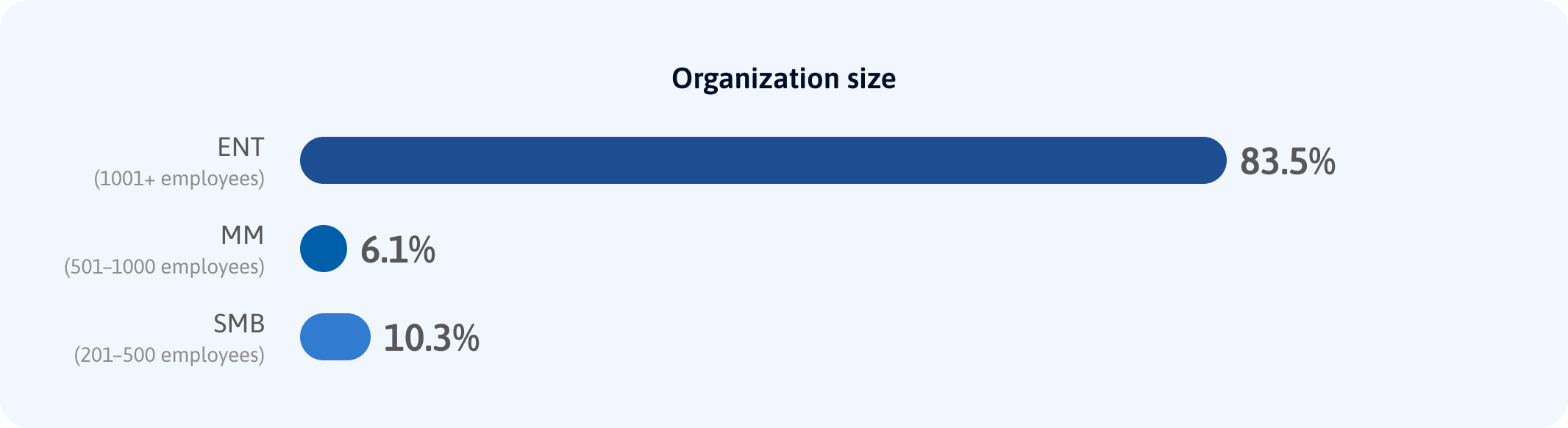

What is the methodology behind the INFUSE Voice of the Buyer 2026 AI Update?

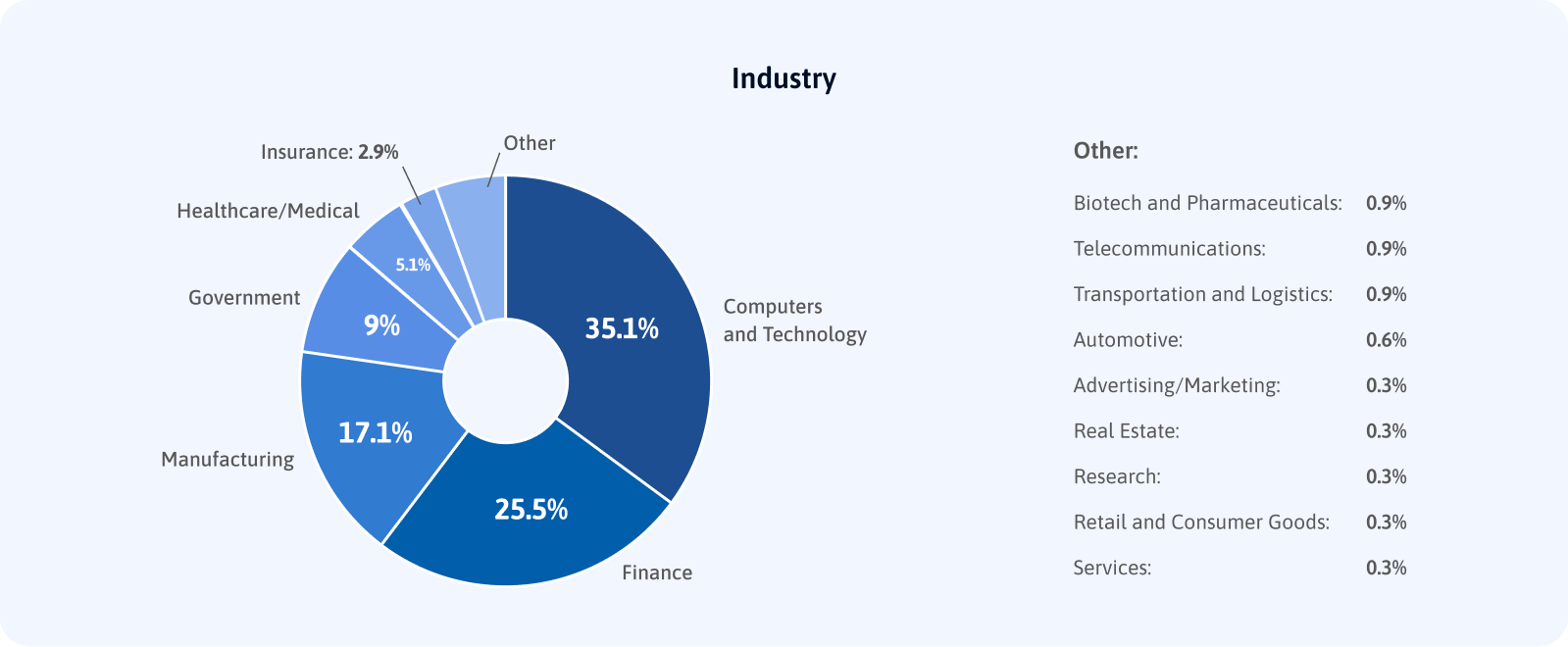

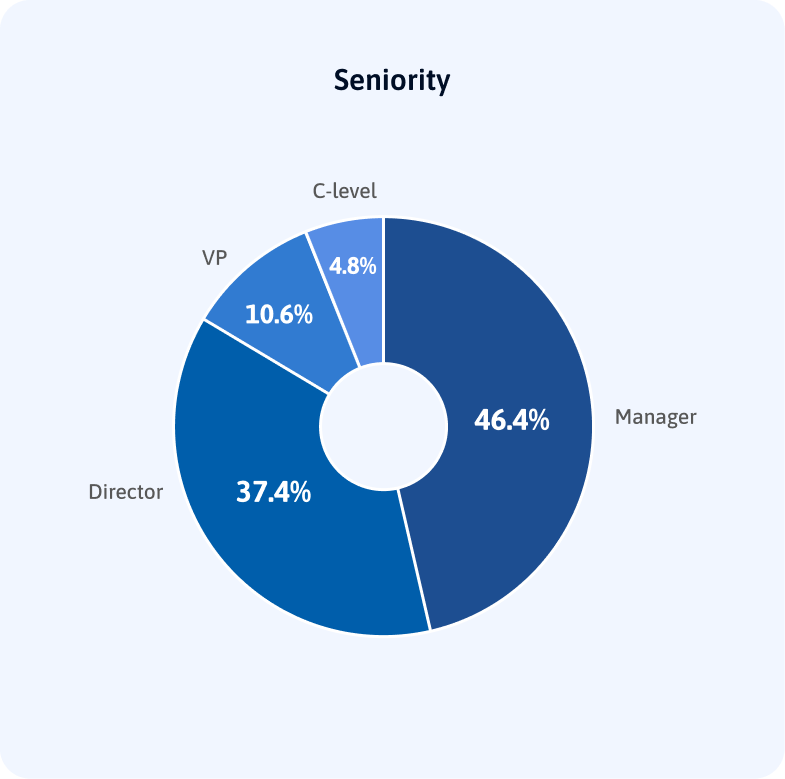

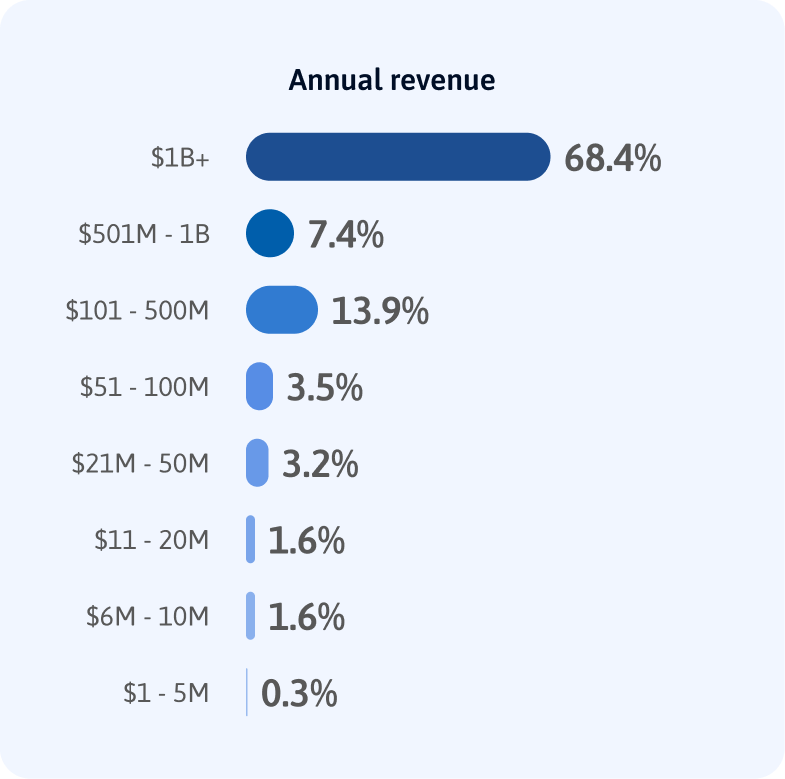

The INFUSE Voice of the Buyer 2026 AI Update is a mid-year survey of 310 B2B technology buyers across 266 companies, 18 countries, and 15 industries, measuring how buyer evaluation of AI solutions has shifted six months after the original INFUSE Voice of the Buyer 2026 study. The update tracks three themes: tech stack consolidation, integration as the new shortlist test, and AI augmentation versus transformation in B2B buyers’ evaluation process.

How is the INFUSE Voice of the Buyer AI Research Reality Check related to INFUSE Outlook 2026?

The INFUSE Voice of the Buyer AI Research Reality Check is the mid-year companion to INFUSE Outlook 2026, measuring what has changed for B2B buyers six months after the original Outlook research identified the Trust Gap as the defining condition of B2B buying in 2026. The VOB 2026 AI Update demonstrates how B2B buyers are adjusting their evaluation processes and expectations when considering AI solutions, revealing a pragmatic approach.